What’s Really Inside Your RRSP — And What the IRS Sees

By: Lucas Wennersten Cross- Border Specialist

Yesterday we established that the TFSA — despite its name — is fully taxable in the United States for dual citizens and US persons. Today the picture becomes more nuanced. The RRSP, unlike the TFSA, does have Treaty protection in the US. But that protection is conditional, requires specific elections to be properly established, carries important limitations that most RRSP holders are unaware of, and interacts with US estate tax in ways that can create significant exposure for HNW dual citizens.

The RRSP is the most valuable registered account most Canadian dual citizens hold. Getting the cross-border treatment right is not a compliance technicality — it is a material planning question that affects how the account should be structured, when and how it should be drawn down, and what it will cost the next generation to inherit.

The Treaty Protection: What It Actually Says

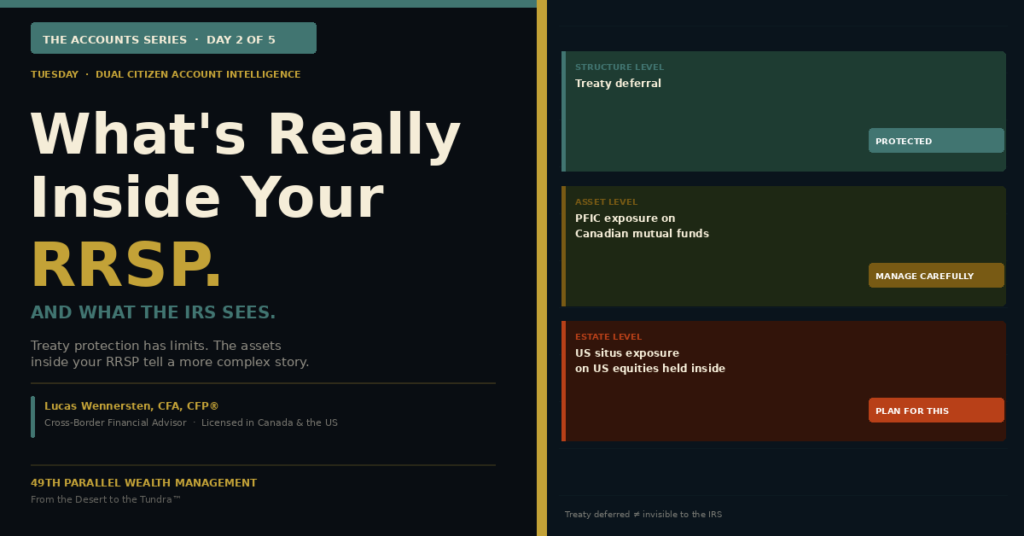

Article XVIII of the Canada–US Tax Treaty covers pension income, including RRSPs and RRIFs. The Treaty grants US tax deferral on income and gains accruing inside an RRSP — meaning that a US person holding an RRSP is not required to include RRSP income in their US taxable income in the year it is earned, provided a proper Treaty election is in place. According to IRS guidance on the Canada-US Tax Treaty and Canadian registered plans, the deferral applies to income, dividends, and capital gains earned inside the account — the same categories that are fully taxable for TFSA holders who lack this Treaty coverage.

This is the meaningful asymmetry between the RRSP and the TFSA for dual citizens. The RRSP is not invisible to the Internal Revenue Service — it must be reported, and its withdrawals are taxed. But its internal growth is protected from annual US taxation in a way the TFSA’s is not.

Three important qualifications apply.

1. The Treaty election must be properly established

Prior to 2014, RRSP holders with US filing obligations were required to file IRS Form 8891 annually to formally elect into the Treaty deferral. Failure to file in any given year — even once — could strip the account of its deferred status retroactively, triggering US tax on all internal growth. In 2014, the Internal Revenue Service issued Revenue Procedure 2014-55, which eliminated Form 8891 and granted automatic retroactive deferral for most RRSP and RRIF holders. This was significant relief for dual citizens who had missed prior-year filings.

However, the Revenue Procedure does not eliminate the need to confirm that the deferral is properly established for your specific account history. Dual citizens who have complex filing histories, gaps in prior-year US returns, or accounts opened during periods of uncertain residency status should have their Treaty election position confirmed by a cross-border tax advisor before assuming the protection applies.

2. Withdrawals are taxable in both countries

The Treaty deferral applies only to income earned inside the account. When funds are withdrawn, they are treated as ordinary income in both Canada (subject to Canadian withholding tax) and the United States. The Canada-US Tax Treaty provides a foreign tax credit mechanism to reduce double taxation on withdrawals — but the interaction between Canadian and US tax rates, the withholding tax treatment, and the timing of withdrawals across the two systems is one of the most consequential sequencing decisions a dual citizen approaching retirement will make.

This is a topic I cover in detail in Crossing the 49th Parallel — specifically the interaction between RRSP drawdown timing, OAS and CPP elections, US Social Security strategy, and the overall cross-border retirement income sequence. The short version: drawing down the RRSP in lower-income years — before OAS, CPP, and Social Security are all in payment — can meaningfully reduce the lifetime tax cost of the account in both jurisdictions. The long version requires a plan that maps both tax systems simultaneously.

3. The Treaty does not protect against US estate tax

This is the gap that surprises most HNW dual citizens. The RRSP’s Treaty deferral applies to income tax during the account holder’s lifetime. It does not shield RRSP assets from US estate tax at death. According to the IRS guidance on US estate tax for non-resident aliens, the RRSP itself is considered a US-situs asset to the extent it holds US-situs investments. More significantly, the entire fair market value of the RRSP may be included in the US taxable estate of a Canadian resident at death under certain circumstances — creating potential double exposure to both Canadian deemed disposition tax and US estate tax on the same account.

|

The RRSP at death: a cross-border estate planning priority On the death of a Canadian RRSP holder who is also subject to US estate tax: · Canada deems the RRSP to have been fully withdrawn at fair market value (deemed disposition) — triggering Canadian income tax · The US may include the same RRSP value in the taxable estate for US estate tax purposes · The Canada-US Tax Treaty provides partial relief through a pro-rata exemption — but for HNW estates the exposure can be material · Proper estate planning — including the use of spousal rollovers, beneficiary designations, and coordinated estate structures — is essential |

What’s Inside the RRSP: The US Situs Asset Problem

Beyond the Treaty deferral question, the composition of what the RRSP holds has direct consequences for US estate tax exposure. This is a dimension of RRSP planning that receives almost no attention in Canadian-only advisory contexts.

US-situs assets held inside an RRSP — shares of US corporations, US-listed ETFs, US Treasury bonds, US real estate investment trusts — are considered US-sited property for estate tax purposes, per the Internal Revenue Service estate tax rules for non-resident aliens. The RRSP wrapper does not change the situs classification of the underlying assets. A Canadian resident who holds USD $500,000 of US equities inside their RRSP has USD $500,000 of US-situs property in their taxable estate, subject to the applicable treaty-based exemption.

For HNW dual citizens with large RRSPs heavily weighted toward US equities — which describes a significant portion of diversified Canadian retirement portfolios — this is a material estate planning consideration. The standard Canadian portfolio construction advice does not account for it.

The planning response is not necessarily to divest all US holdings from the RRSP. It is to understand the exposure, quantify it as part of an overall estate plan, and structure the estate accordingly — which may include rebalancing toward Canadian or non-US assets inside the registered account, or coordinating the RRSP structure with a broader estate plan that addresses the US situs exposure through other mechanisms.

The PFIC Question Inside the RRSP

Yesterday we covered the Passive Foreign Investment Company rules in the context of the TFSA, where the absence of Treaty protection creates direct annual PFIC tax exposure. Inside the RRSP, the analysis is different but not irrelevant.

The Treaty deferral generally suspends the annual PFIC tax accrual on Canadian mutual funds held inside an RRSP — because the income is deferred, the annual PFIC accrual mechanism does not engage. However, this protection is contingent on the Treaty election being properly established and maintained. For dual citizens whose Treaty election history has gaps or uncertainties, the PFIC exposure inside the RRSP is a secondary risk that cannot be ignored.

When RRSP funds are ultimately withdrawn, the accumulated gains are treated as ordinary income — bypassing the PFIC excess distribution rules that would otherwise apply. This is one of the meaningful planning advantages of the RRSP Treaty protection over the unprotected TFSA: even with Canadian mutual fund holdings, the tax treatment on eventual withdrawal is more predictable and generally less punitive.

Cross-Border Account Treatment Comparison

| Account | Treaty coverage | US tax treatment | Annual US reporting |

| RRSP / RRIF | Yes — explicit | Tax-deferred until withdrawal | FBAR if >$10K; no Form 3520 |

| TFSA | None | Fully taxable annually | FBAR + potential Form 3520 |

| Non-registered | N/A | Taxable (dividends, gains) | FBAR if >$10K |

| Canadian pension | Partial | Treaty-reduced withholding | FBAR if >$10K |

| US 401(k)/IRA | N/A | Tax-deferred as normal | Standard US reporting |

Note: This table represents general principles. Individual circumstances, Treaty election status, and account composition significantly affect the actual treatment. This is not tax advice — consult a dual-licensed cross-border advisor.

The Withdrawal Sequencing Decision: The Highest-Stakes RRSP Question

For a dual citizen approaching retirement, the single most consequential RRSP question is not “what does it hold?” It is “when do I draw it down, and in what order relative to my other income sources?”

The conventional Canadian retirement planning advice is to defer RRSP/RRIF withdrawals as long as possible, drawing on non-registered assets first and allowing the registered account to compound. For a Canadian-only perspective, this often makes sense. For a dual citizen, it requires a more layered analysis.

- The RRSP conversion to RRIF must occur by the end of the year the account holder turns 71 — after which mandatory minimum withdrawals begin

- Each RRIF withdrawal is taxable in both Canada and the US, with the foreign tax credit reducing but not eliminating double taxation in high-income years

- US Social Security, CPP, and OAS payments are all taxable income in both jurisdictions — once all three are in payment, the marginal rate on additional RRIF withdrawals can be significantly higher

- The WEP repeal (Social Security Fairness Act 2025) changed the calculation for dual citizens receiving both CPP and Social Security — the previous offset that reduced Social Security for CPP recipients no longer applies, increasing combined income and the tax bracket pressure on RRIF withdrawals

- In lower-income years before CPP, OAS, and Social Security are all active, strategic RRSP/RRIF withdrawals — sometimes called “RRSP meltdown” strategy — can meaningfully reduce the lifetime cross-border tax cost of the account

This is the kind of integrated analysis that cannot be done properly with one advisor on each side of the border working independently. The sequencing decision requires a simultaneous view of both tax systems, both sets of government benefits, and the full retirement income picture across both countries — exactly the kind of Canada–US retirement strategy that defines what a dual-licensed cross-border advisor does differently.

Client ScenarioPatricia is a 67-year-old dual citizen who retired from a career spanning both Toronto and Chicago. She holds a CAD $680,000 RRSP, a USD $240,000 IRA, and non-registered accounts in both countries. She began drawing Canadian CPP at 65 and has deferred US Social Security to 70. Her Canadian advisor has recommended holding the RRSP as long as possible. Her US accountant has processed her returns but has not engaged with the retirement income sequencing question. In her first cross-border planning review, it became clear that the two-year window between now and her Social Security commencement represented a significant opportunity to draw down RRSP assets at a materially lower combined rate than she will face once Social Security begins. The projected tax saving from drawing strategically over that window, versus deferring, exceeded USD $40,000 in present value terms. Neither advisor had identified it independently. The number only became visible when both tax systems were modelled together. |

Frequently Asked Questions

Is an RRSP protected from US taxation for dual citizens?

Yes — but conditionally. The Canada–US Tax Treaty grants RRSP and RRIF holders US tax deferral on income earned inside the account. This protection requires a proper Treaty election to be established, does not apply to RRSP withdrawals (which are taxable in both countries), and does not shield against US estate tax on US-situs assets held inside the account.

What US reporting is required for an RRSP?

At minimum: FBAR (FinCEN 114) if total foreign financial accounts exceed USD $10,000; Form 8938 if foreign financial assets exceed FATCA thresholds. The previously required annual Form 8891 was eliminated by Revenue Procedure 2014-55, which granted automatic retroactive deferral. Dual citizens should confirm their Treaty election history with a cross-border tax advisor.

Are Canadian mutual funds inside an RRSP subject to PFIC rules?

The Treaty deferral generally shields RRSP holdings from annual PFIC taxation while funds remain in the account. However, this protection is conditional on proper Treaty elections being in place. Confirm your election status with a dual-licensed cross-border advisor.

Do US-listed stocks inside my RRSP create US estate tax exposure?

Yes. US-situs assets — including US equities, US ETFs, and US bonds — held inside an RRSP are considered US-sited property for estate tax purposes. The RRSP wrapper does not change the situs classification of the underlying assets.

How should a dual citizen think about RRSP withdrawal sequencing?

The sequencing question — when to draw down the RRSP relative to CPP, OAS, Social Security, and other income sources — is one of the most consequential retirement planning decisions for a dual citizen. The optimal strategy requires modelling both tax systems simultaneously. This is covered in depth in

Crossing the 49th Parallel (crossingthe49thparallel.com) and is best addressed through a coordinated Canada–US retirement strategy review with a dual-licensed advisor.

|

Lucas Wennersten’s book Crossing the 49th Parallel covers the full landscape of Canada–US financial planning — from account strategy and tax coordination to estate planning and retirement income sequencing. Written for dual citizens, cross-border families, and anyone navigating life between two countries, it is the practical guide that does not exist in a single advisor meeting. Available at crossingthe49thparallel.com |

About the Book

About the Book

Has your RRSP ever been reviewed with both Canada and the US in the picture?Most dual citizens have had their RRSP reviewed by a Canadian advisor only. The cross-border dimension — Treaty elections, US situs asset exposure, withdrawal sequencing across two tax systems — rarely comes up in a standard Canadian retirement planning conversation. Lucas Wennersten holds dual credentials as a CFA and CFP® in both Canada and the United States and works exclusively with clients whose financial lives require both perspectives simultaneously. Read more at Crossing the 49th Parallel: A Retirement Planning Guide for Moving Across the Canada- U.S. Border — available at crossingthe49thparallel.com and Amazon Book a complimentary consultation at 49thparallelwealthmanagement.com/contact-us/ |